A joint Visa and Artemis analysis published on July 14 divides this emerging market into two categories. The first resembles […]

The post How Stablecoins Could Become AI’s Native Payment Rail appeared first on Coindoo.

A joint Visa and Artemis analysis published on July 14 divides this emerging market into two categories. The first resembles ordinary online commerce, with an agent booking travel or managing a subscription for a person. The second consists of frequent software-to-software payments, often worth less than $1, for resources such as API calls, data and short periods of computing time.

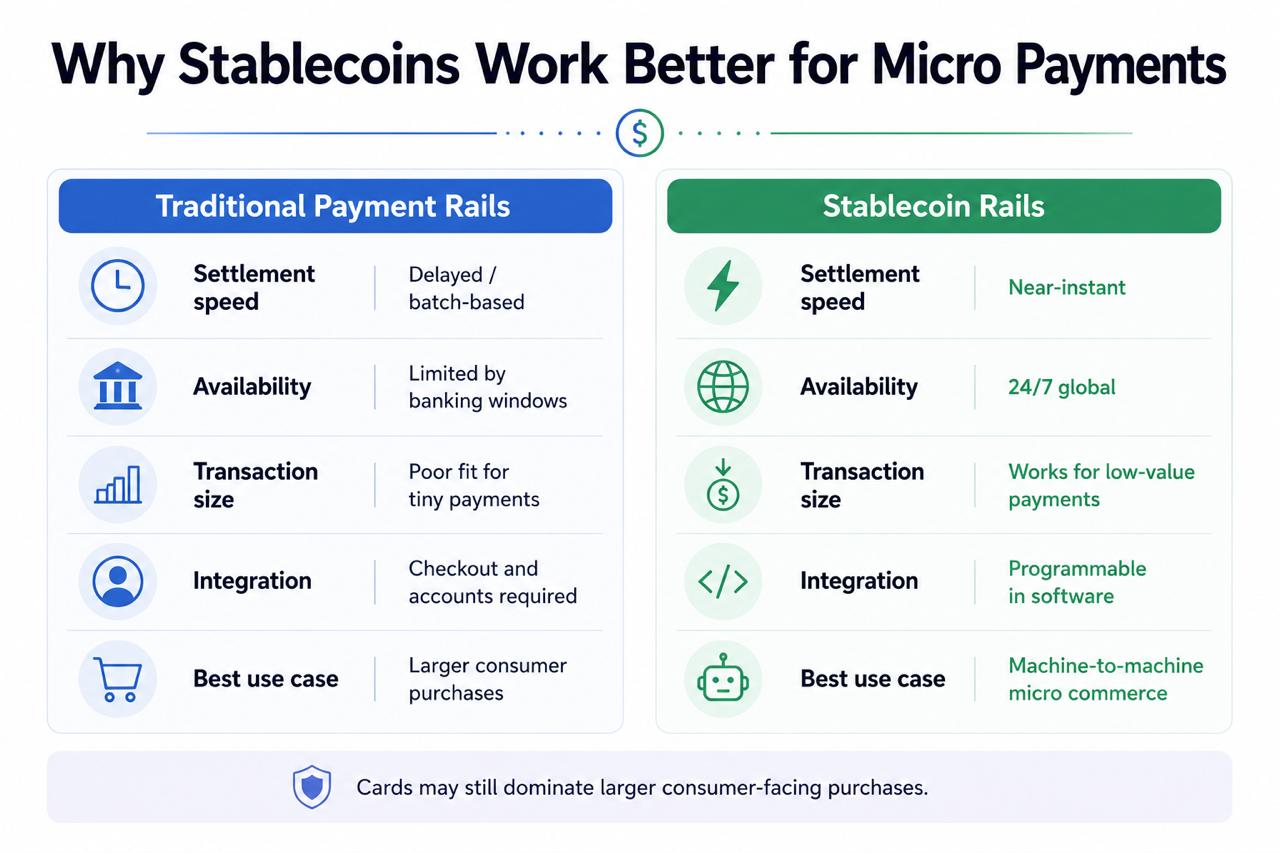

Stablecoins have an early advantage in the second category. Their programmable settlement and low blockchain fees can support transactions too small or frequent for conventional checkout systems. That does not mean cards and bank payments will disappear. The more likely outcome is a multi-rail economy in which agents choose different payment methods according to the size, purpose and risk of each transaction.

Key Takeaways

- Visa expects AI agents to use stablecoins.

- Sub-dollar payments suit machine-to-machine commerce best.

- Stablecoins enable instant, low-cost programmable settlement.

- x402 embeds payments into standard web requests.

- MPP supports both crypto and fiat rails.

- Cards remain useful for larger agent purchases.

- Security, identity and disputes remain unresolved.

AI Commerce Is Splitting Into Two Markets

Not every payment initiated by an AI agent requires a new financial system. When an agent purchases a flight, renews business software or orders goods for a person, the transaction still resembles conventional e-commerce. The amount is large enough to support existing authorization, fraud detection, refund and chargeback processes.

Visa describes this as macro commerce. The agent changes who navigates the purchase, but the underlying payment remains a familiar consumer or business transaction. Card networks are already developing tools that allow authorized agents to use payment credentials while preserving spending controls and merchant verification.

Micro commerce has different economics. An agent may need one database query, three minutes of GPU capacity or temporary access to a software function. The service could cost $0.05 rather than $50, with the agent repeating similar purchases hundreds or thousands of times.

The Visa analysis says these machine-to-machine payments frequently fall below $1. Newer blockchain networks have reduced settlement costs to fractions of a cent, making payments between approximately one cent and one dollar practical in situations where processing overhead would otherwise consume much of the transaction value.

The distinction points toward two parallel payment layers. Cards may remain well suited to agents buying products for people, while stablecoins could handle the smaller transactions that software makes to other software.

What a Five-Cent Agent Payment Could Look Like

An agent purchasing information from a paid data service could complete the entire exchange through an open payment protocol:

- The agent determines that it needs a specific dataset to complete a task.

- It finds an API offering the required information for $0.05.

- The service returns a machine-readable payment request.

- The agent checks the price against its authorized budget and sends the stablecoin payment.

- The service verifies settlement and immediately returns the requested data.

No account, monthly subscription or manually entered card number is required. The agent purchases one unit of value precisely when it needs it.

Traditional Checkout Was Designed for People

The limitation is not that existing payment systems cannot process transactions initiated by software. It is that their commercial workflows were built around human behaviour.

Stripe noted when it introduced its Machine Payments Protocol that a normal online purchase may require an agent to create an account, navigate a pricing page, choose a subscription plan, enter payment details and establish a billing relationship. Those steps are manageable for a person making an occasional purchase but become a bottleneck when software needs one small service for a few seconds.

Subscriptions are also a poor fit for agents that interact with many providers unpredictably. An autonomous research system might use one data source today and a different one tomorrow. Requiring it to maintain an account and monthly plan with every potential provider would recreate the same friction that automation is supposed to remove.

Machine commerce instead requires the price, authorization and payment instructions to be readable by software. The transaction must be small enough to match the resource being consumed and fast enough that settlement does not interrupt the agent’s task.

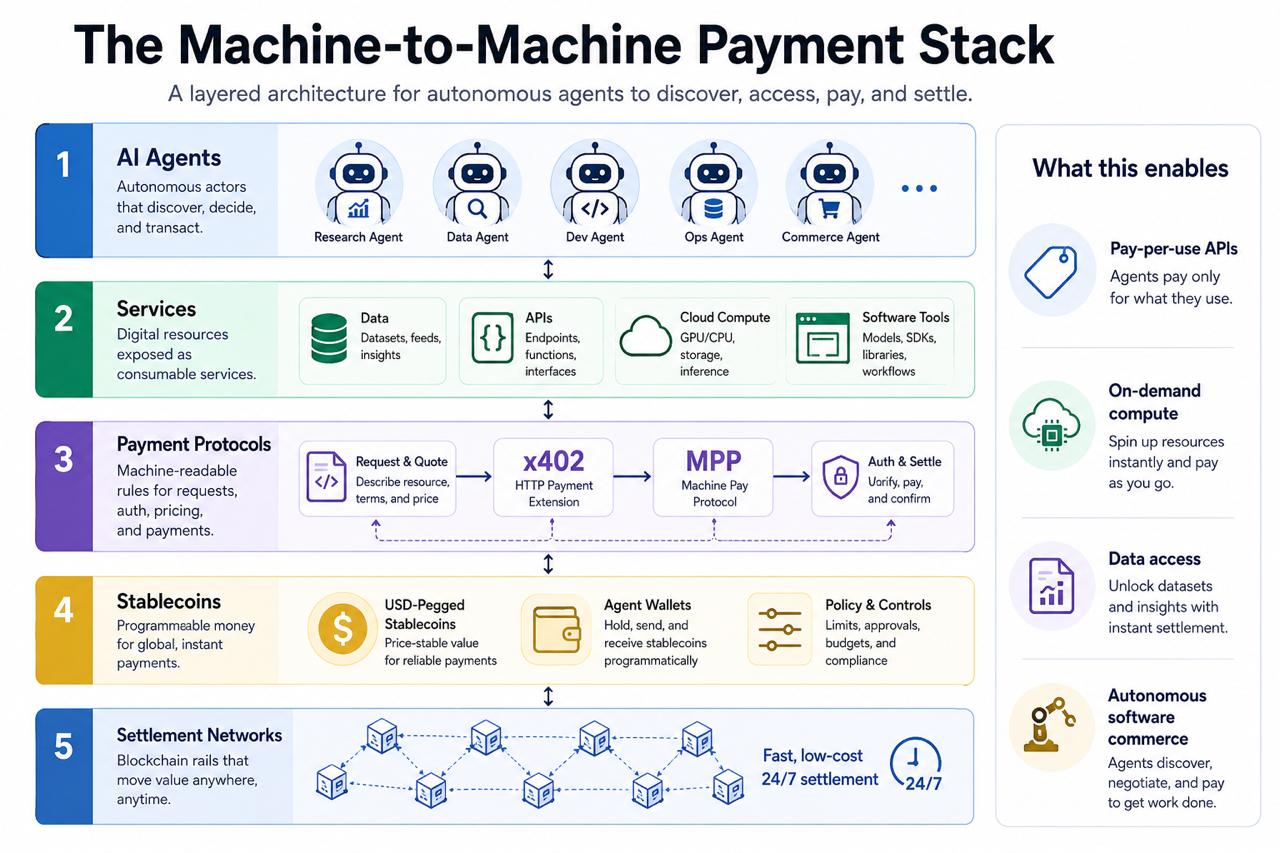

x402 Makes Payment Part of a Web Request

The development of open payment standards suggests that machine payments are moving beyond isolated experiments. On July 14, 2026, the Linux Foundation announced the operational launch of the x402 Foundation, placing the protocol under formal, vendor-neutral governance.

x402 uses the internet’s existing HTTP structure to include payment within the exchange between a client and a server. A service can respond to a request with payment instructions, while the agent can authorize the charge and provide proof of payment before receiving the resource.

The protocol takes its name from the HTTP 402 “Payment Required” status code. According to the official x402 documentation, it allows APIs and online services to charge for individual requests without requiring conventional accounts, sessions or credential management.

The comparison with an “HTTP for payments” is useful but incomplete. HTTP standardized how information moves across the web; x402 is attempting to standardize how a payment request and its response are communicated. It does not require every transaction to use the same company, blockchain or payment asset.

The x402 Foundation launched with 40 participating organizations across payments, cloud infrastructure, AI and blockchain. Its membership includes Visa, Mastercard, American Express, Stripe, Coinbase, Cloudflare, Amazon Web Services, Google, Circle and Shopify. The variety is important because the protocol is designed to support payment methods ranging from stablecoins to traditional cards rather than locking the machine economy into one rail.

Cloudflare Is Turning the Protocol Into Infrastructure

Cloudflare has already announced a practical implementation. Its forthcoming Monetization Gateway will allow customers to charge for web pages, datasets, APIs and Model Context Protocol tools protected by Cloudflare.

Payments will settle in stablecoins through x402 at launch. Cloudflare will handle payment verification and access enforcement at the network edge, reducing the need for each publisher or developer to build an independent blockchain payment system.

The model could change how online information is monetized. A provider would no longer need to choose only between advertising, a monthly subscription or free access. It could sell a single article, database query or software action directly to an agent at the moment of use.

Why Stablecoins Fit the Micro-Payment Layer

Stablecoins combine the programmability of blockchain networks with a unit of account intended to track currencies such as the U.S. dollar. An agent can therefore evaluate a price, compare it with its budget and settle the transaction without managing the volatility of an unbacked crypto asset.

The institutional infrastructure supporting this model is also expanding. Open USD launched with backing from more than 140 financial and crypto companies, including Visa, Mastercard and BlackRock, showing that major payment and asset-management firms increasingly view stablecoins as infrastructure for broader internet commerce, including future machine-to-machine transactions.

Their strongest advantage is not simply that they operate continuously. It is that payment instructions, authorization and settlement can be incorporated into the same software workflow that requests the underlying service.

- Granular pricing: Developers can charge for one API call, one computation or a small segment of data rather than requiring a subscription.

- Programmatic settlement: An agent can initiate and verify a payment without navigating a consumer checkout page.

- Global availability: The same technical rail can operate across time zones without being limited to local banking hours.

- Automated accounting: Each purchase can produce a verifiable digital record that software can reconcile against the agent’s budget.

Stripe’s machine-payment documentation already supports individual charges as low as 0.01 USDC. That price level allows services to sell resources in units that would have little reason to exist under a conventional checkout model.

The Machine Economy Changes What Can Be Sold

Machine payments do more than automate an existing transaction. They allow businesses to divide digital products into much smaller units and price them according to actual use.

- Computing capacity: An agent could rent GPU resources for several minutes, complete one task and stop paying when the workload ends.

- Data access: A research agent could purchase one real-time market figure, satellite image or private database result.

- Web infrastructure: An agent could pay for a single browser-rendering session rather than maintaining a monthly account.

- Software functions: Developers could charge separately for individual model calls, searches, translations or verification requests.

Once agents can discover prices and settle automatically, providers could also adjust prices in response to demand. Computing capacity might become more expensive during periods of congestion, while rarely used datasets could be sold cheaply without requiring a salesperson or bilateral contract for every customer.

Open protocols reduce the technical integration required before two systems can transact. They do not remove the need for contracts, compliance or commercial accountability in higher-risk relationships, but they can make low-value digital services accessible without a separate negotiation between every buyer and seller.

MPP Shows Stablecoins Will Not Be the Only Rail

x402 is not the only standard being developed. Stripe and Tempo launched the Machine Payments Protocol, or MPP, in March 2026 to support programmatic microtransactions, recurring payments and other agent-driven purchases.

MPP can coordinate payments through stablecoins as well as fiat-based methods supported by Stripe. This reflects a broader industry direction: agents may not care which rail completes a payment as long as it meets their requirements for cost, speed, reliability and authorization.

Adoption remains small compared with the infrastructure being built. Circle and Stripe are developing stablecoin infrastructure for autonomous AI payments, while roughly 40,000 on-chain agents account for only 0.0001% of stablecoin settlement volume. Agentic commerce has therefore moved beyond theory but remains economically insignificant compared with the wider stablecoin market.

Visa’s position is similarly multi-rail. Its research does not argue that stablecoins will replace cards throughout agentic commerce. Card infrastructure may remain better suited to larger purchases made on behalf of consumers, while machine-native settlement becomes more relevant for software-to-software transactions.

The claim that stablecoins will become the native payment rail of the AI economy is therefore most credible when applied to micro commerce. A $0.03 API call and a $3,000 airline booking create different risks and require different protections. There is little reason to expect both to use an identical payment system.

Autonomous Payments Create New Risks

Giving an AI agent control over money introduces problems that faster settlement alone cannot solve. A compromised agent could make unauthorized purchases at machine speed, while a poorly configured budget could turn a small recurring charge into a large cumulative loss.

- Identity and authorization: Merchants need to know whether an agent is legitimate and whether its user approved the transaction.

- Spending controls: Agents require limits covering individual purchases, total budgets, approved merchants and permitted services.

- Dispute resolution: Existing chargeback processes were not designed for chains of agents completing thousands of transactions per hour.

- Protocol fragmentation: Competing standards could recreate closed payment ecosystems unless x402, MPP and future systems remain interoperable.

- Settlement risk: A stablecoin payment still depends on the issuer, its reserves, the selected blockchain and the security of the wallets involved.

Visa’s Intelligent Commerce framework is focused on bringing familiar controls into agent-led transactions, including authenticated credentials, spending limits, approval workflows and trusted identity signals.

Disputes may be harder to adapt. The Visa and Artemis report notes that conventional evidence and chargeback windows assume a human-speed purchase with a recognizable order. When multiple agents pay one another through a chain of services, determining which transaction failed and who should absorb the loss becomes more difficult.

Stablecoins also introduce risks beyond the agent itself. The International Monetary Fund has warned that their value can come under pressure if reserve assets lose value or confidence in redemption weakens. Low-cost settlement does not eliminate issuer, liquidity, legal or operational risk.

Developers, Businesses and Investors

- For developers: Consider building x402-compatible endpoints and testing pay-per-use access for APIs, data and software functions. Machine payments could make usage-based pricing more practical than requiring every agent to maintain a subscription.

- For businesses: Treat AI agents as potential customers, not only as interfaces for human users. Digital assets such as datasets, computing capacity and specialized tools could be packaged into units that agents can discover, purchase and consume autonomously.

- For investors: The infrastructure layer may be more important than any single AI-payment application. Wallets, identity systems, stablecoin issuers, payment protocols and platforms supporting x402 or MPP will determine whether machine commerce can scale securely.

Stablecoins Have an Edge, Not a Monopoly

The early evidence supports a narrower conclusion than the claim that all AI commerce will move onto crypto rails. Stablecoins appear particularly well suited to the emerging market for sub-dollar transactions between software systems, where conventional accounts, subscriptions and checkout procedures create disproportionate friction.

Cards and fiat payments retain advantages in consumer protection, acceptance, credit and dispute handling. Stablecoins offer different strengths: granular pricing, programmable authorization and settlement that can operate within an automated workflow.

The decisive shift is not an AI agent receiving its own bank account. It is the development of open standards that allow software to discover a service, understand its price, pay within an approved budget and receive the result without human intervention.

If x402, MPP and related systems achieve broad adoption, stablecoins could become an invisible settlement layer beneath parts of the internet. Users may never see the wallet or blockchain involved. They will simply see agents that can purchase the data, computing power and digital services required to complete a task.

The information provided in this article is for educational purposes only and does not constitute financial, investment or trading advice.

The post How Stablecoins Could Become AI’s Native Payment Rail appeared first on Coindoo.

Source: https://coindoo.com/stablecoins-become-ai-native-payment-rail/

More Crypto News

Check our Market Overview

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research (DYOR).