Key Takeaways The trial is limited to employees of the participating companies, making it a controlled technical test rather than […]

The post Japanese Convenience Store Tests Stablecoin Payments appeared first on Coindoo.

Key Takeaways

- The trial is limited to employees of the participating companies, making it a controlled technical test rather than a measure of wider consumer demand.

- Japan’s ¥1 million restriction for foreign stablecoins generally applies to individual transfers through registered intermediaries, not as a universal daily spending cap.

- Japan, Singapore, and Hong Kong are developing different stablecoin models spanning retail checkout integration, issuer licensing, and institutional settlement.

Lawson, one of Japan’s largest convenience-store chains, will run a yen-denominated stablecoin payment pilot in August 2026 at its Takanawa Gateway City store in Tokyo. The company operates 14,697 stores across Japan, selling everyday products and providing services such as ATMs, ticketing, bill payments, and parcel collection.

That nationwide presence makes Lawson a meaningful testing ground for whether stablecoins can move beyond specialist crypto platforms and become usable for routine purchases. The payment will be processed through Lawson’s existing point-of-sale system rather than a separate crypto terminal, reducing the amount of new hardware and operational change required at checkout.

The agreement was signed by Lawson, KDDI, and digital-asset infrastructure company HashPort on July 10 and announced by HashPort on July 13. The August experiment will be restricted to employees of the participating companies, so its first objective is to assess technical and operational viability rather than broad consumer adoption.

Although some reports have identified the payment asset as JPYC, the primary announcement refers only to a Japanese yen stablecoin and does not name its issuer. It also does not describe the pilot as the first stablecoin POS integration in Japan.

The Register, Not the Token, Is the Main Experiment

Customers participating in the trial will open HashPort’s non-custodial mobile wallet and display a payment code at checkout. The cashier will scan it using the same register equipment used for Lawson’s other payment methods.

On the merchant side, HashPort Wallet for Biz will handle the stablecoin payment without requiring the individual store to open and operate its own blockchain wallet. Canal Payment Services, the payment-processing subsidiary of KDDI, will connect the code-payment infrastructure with Lawson’s register system.

The pilot will measure several practical variables:

- Transaction performance: How long authorization and settlement take, particularly during periods of heavier customer traffic.

- Cashier operations: Whether employees need additional steps, training, or manual intervention to complete a payment.

- Wallet usability: Whether customers can generate and present the payment code without slowing the checkout queue.

- Reconciliation: Whether the payment can be matched accurately with the customer’s basket, transaction timestamp, refund process, and Lawson’s internal accounting data.

Connecting the payment directly to the POS system keeps it linked with the underlying purchase record rather than leaving it as an isolated blockchain transfer. Lawson could therefore retain the inventory, timing, and basket-level visibility it receives from card and existing QR-code payments.

The company has not announced a broader rollout. Its nationwide network gives the technology considerable theoretical scale, but the August test must first show that the payment can fit into routine store operations without creating additional friction for customers, cashiers, or accounting teams.

Japan Has Already Built the Legal Route for Stablecoin Payments

Japan’s revised Payment Services Act established a dedicated category for fiat-referenced stablecoins known as electronic payment instruments. The framework took effect in June 2023 and separates the entities allowed to issue stablecoins from the intermediaries permitted to distribute, exchange, or transfer them.

Under the Financial Services Agency’s regulatory framework, issuers must operate as banks, fund transfer service providers, or trust companies, depending on the token’s legal structure. Intermediaries handling electronic payment instruments must separately register and comply with custody, anti-money-laundering, disclosure, and asset-protection requirements.

The reserve rules are more nuanced than a universal requirement to hold every stablecoin’s backing in the same assets. A subsequent amendment widened the permitted reserve management options for trust-structured stablecoins.

Previously, the full backing for this type of token generally had to remain in demand deposits. The revised provisions allow up to 50% to be placed in principal-protected assets, including cancellable fixed-term deposits and Japanese or US government securities with remaining maturities of three months or less, according to FSA legislative materials.

The change does not apply identically to every stablecoin issued under Japan’s other legal structures.

That distinction affects how issuers generate reserve income, manage liquidity, and guarantee redemption at par. It also means the strength of a Japanese stablecoin cannot be assessed solely from its yen peg; the issuer’s legal category and reserve arrangement remain material.

Lawson’s pilot is arriving as Japan’s broader crypto market moves further into regulated, mainstream finance. In June 2026, Ripple’s dollar-backed RLUSD became legally available in the country through SBI VC Trade, while a Japanese pension fund serving small and mid-size businesses disclosed plans to allocate about 1% of its assets to crypto as a hedge against yen weakness. Japan’s lower house also advanced legislation moving crypto under securities law and opening a legal path for spot ETFs and tax reform. Together, these developments show that retail payments, institutional investment, and market regulation are progressing in parallel rather than as isolated experiments.

The ¥1 Million Rule Is Not a Universal Daily Limit

Japan places additional restrictions on registered service providers handling foreign-issued electronic payment instruments such as dollar-denominated stablecoins.

The FSA’s supervisory guidelines generally require an intermediary to limit an individual foreign-stablecoin transfer to ¥1 million (around $6,170). The rule is commonly described as a daily transaction cap, but the official language is structured around each transfer.

Regulators have also indicated that dividing one commercial payment into several consecutive transactions below ¥1 million could be treated as an attempt to evade the restriction.

For Lawson, the ceiling is unlikely to affect ordinary purchases. The operational consequences become more relevant for merchants selling high-value electronics, luxury products, or large tourist orders.

Such retailers would need systems capable of detecting restricted payments before authorization rather than relying on cashiers to recognize them manually. Refunds, partial cancellations, accumulated customer balances, and attempts to split a purchase would also need to be handled without breaching the intermediary’s obligations.

A domestic yen stablecoin is not automatically free from every transaction or redemption restriction. Its practical limits depend on whether it is issued by a bank, trust company, or fund transfer service provider, as well as the specific terms imposed by the issuer and wallet service.

The regulatory advantage is therefore structural rather than an unconditional exemption for every yen-denominated token.

Three Routes Are Emerging Into Japanese Commerce

The Lawson trial is part of a broader effort to determine which stablecoin architecture can operate inside Japan’s established payment system. The leading projects are approaching that objective from different directions.

- Domestic retail payments: Lawson, KDDI, and HashPort are testing whether a yen stablecoin can be incorporated into an established convenience-store payment environment.

- Foreign stablecoins for inbound consumers: Payment gateway Netstars launched a USDC retail payment service at selected Haneda Airport stores in December 2025. Customers present a USDC payment code, which is scanned through the company’s StarPay infrastructure.

- Bank-issued stablecoins: Japan’s FSA established the Payment Innovation Project with Mizuho, MUFG, SMBC, Mitsubishi Corporation, Mitsubishi UFJ Trust and Banking, and Progmat. The project examines whether several banking groups can jointly issue and operate stablecoins while meeting existing legal and supervisory requirements.

These are not interchangeable products. A domestic retail token prioritizes predictable yen value and integration with local accounting. A foreign token such as USDC is more relevant to tourists and cross-border users but faces additional intermediary restrictions. A bank-issued token could carry stronger institutional distribution while requiring more complex coordination between issuers.

Lawson’s trial is therefore one part of an emerging payment stack rather than evidence that Japan has already selected a dominant stablecoin model.

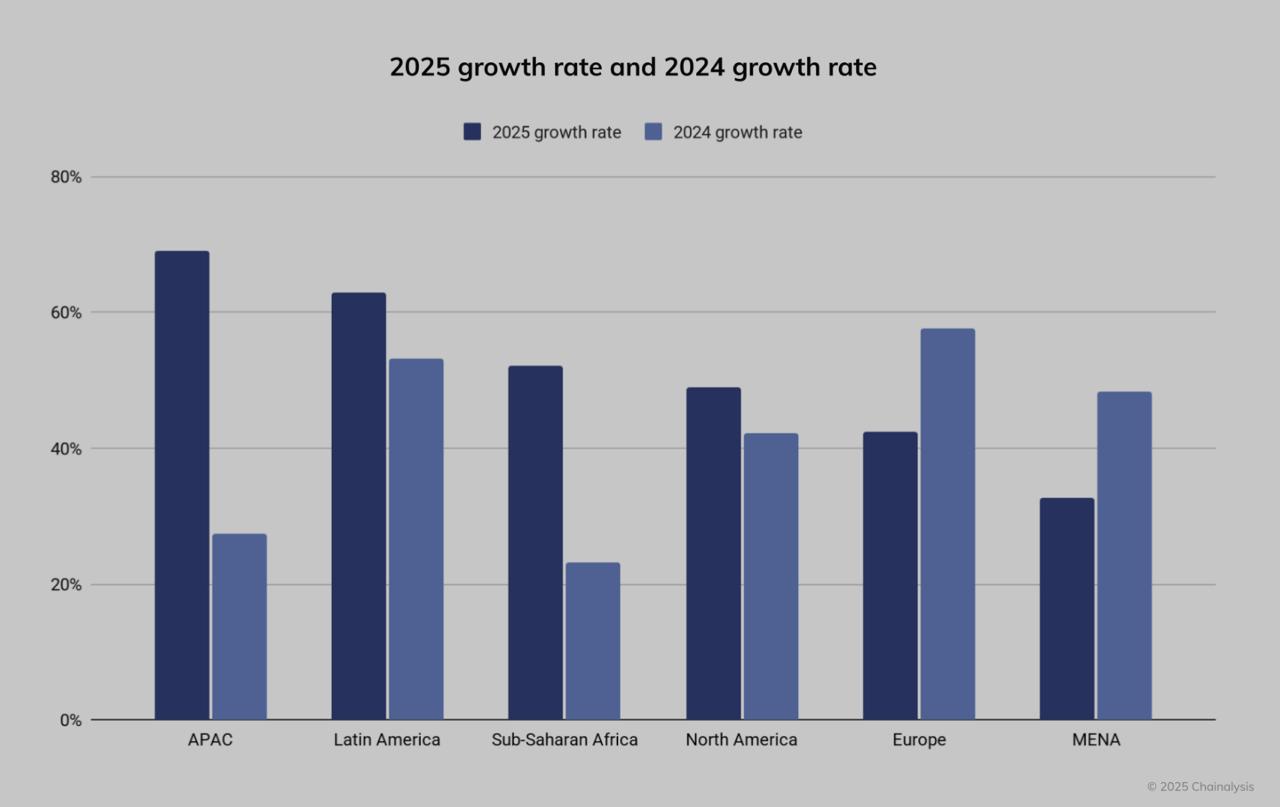

Asia Is Not Converging on One Regulatory Design

Asia-Pacific recorded the fastest growth in on-chain crypto activity among the regions tracked by Chainalysis, with transaction value increasing 69% year over year to approximately $2.36 trillion during the 12 months ending in June 2025, according to the company’s Global Crypto Adoption Index.

That growth does not mean stablecoin regulation or retail adoption is developing uniformly across the region.

Singapore has finalized a policy framework for single-currency stablecoins issued domestically and pegged to the Singapore dollar or a G10 currency. The framework includes full backing with low-risk liquid assets, minimum base capital of S$1 million, and redemption at par within five business days.

Its legal status should not be overstated. The Monetary Authority of Singapore’s finalized framework sets out the planned regulatory model, but its implementation still depends on the relevant legislation and detailed regulatory requirements taking effect.

Hong Kong has moved further into implementation. Its fiat-referenced stablecoin licensing regime took effect on August 1, 2025. Licensed issuers must maintain reserve assets at least equal to the outstanding stablecoin value, segregate those assets, provide redemption at par, and use qualified custodians accepted by the Hong Kong Monetary Authority.

The requirements, licensing process, and supporting materials are available through the HKMA’s official stablecoin issuer portal.

Singapore’s BLOOM initiative occupies another layer of the market. It supports industry experiments involving tokenized bank liabilities and regulated stablecoins for settlement, particularly institutional and cross-border use cases.

Official material does not establish BLOOM as a live Singapore–Thailand consumer payment corridor with confirmed expansion into Japan and Taiwan.

The regional divide is therefore not simply between stricter and looser regulation. Japan is testing how regulated digital money fits into established retail infrastructure, Hong Kong has prioritized a dedicated issuer-licensing regime, and Singapore is combining a single-currency stablecoin framework with broader institutional settlement experiments.

What Would Turn One Store Into a Scalable Payment Model

The August pilot will produce stronger evidence if Lawson publishes measurable results rather than only confirming that the transactions were completed.

The most useful disclosures would include average completion time, failure and retry rates, refund performance, reconciliation accuracy, and the total merchant cost compared with existing card and QR-code payments.

The controlled format also leaves several commercial questions unresolved. Company employees may already understand the wallet, receive setup instructions, and have direct access to technical support. Ordinary customers introduce less predictable behavior, including incomplete onboarding, lost credentials, incorrect networks, insufficient balances, and hesitation at checkout.

A technically successful transaction is therefore a lower bar than a commercially successful payment method.

Lawson’s pilot becomes meaningful if the blockchain component disappears into the background: customers complete payments without added friction and transactions reconcile without manual work. Failure at any of those points would limit the value of Lawson’s national scale, regardless of how quickly the token settles on-chain.

The information provided in this article is for informational purposes only and does not constitute financial, investment, or legal advice.

The post Japanese Convenience Store Tests Stablecoin Payments appeared first on Coindoo.

Source: https://coindoo.com/japanese-convenience-store-tests-stablecoin-payments/

More Crypto News

Check our Market Overview

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research (DYOR).