Key Takeaways NYSE has dropped the 25,000-contract cap on Bitcoin and Ethereum ETF options, aligning them with standard commodity ETF […]

The post NYSE Removes Position Limits on Bitcoin and Ether ETF Options – What Actally Changed appeared first on Coindoo.

Key Takeaways

- NYSE has dropped the 25,000-contract cap on Bitcoin and Ethereum ETF options, aligning them with standard commodity ETF rules

- FLEX options are now available, giving institutions customizable terms previously only found in OTC markets

- Nasdaq, Cboe, and MIAX have made identical moves – virtually every major regulated venue now follows the same framework

- The SEC has shifted to generic listing standards for spot crypto ETFs, ending case-by-case approvals

NYSE Arca and NYSE American have scrapped the 25,000-contract position and exercise limits that applied to options on 11 spot crypto ETFs – a cap that was only put in place in late 2024. The SEC granted an immediate waiver, meaning the change didn’t sit in a queue – it went live.

The funds affected include some of the biggest names in the space: BlackRock’s iShares Bitcoin Trust (IBIT), Fidelity’s Wise Origin Bitcoin Fund, and Grayscale’s Bitcoin and Ethereum Trusts, among others. Under the new framework, position limits are set by standard exchange rules – where large, sufficiently liquid ETFs can qualify for thresholds of 250,000 contracts or more. For context, that ceiling for IBIT alone would represent roughly 2.89% of its outstanding shares.

This isn’t just a NYSE story. Nasdaq removed the same 25,000-contract restriction across its platforms effective January 21. Cboe filed its own rule changes on February 24, covering 12 spot Bitcoin and Ether ETFs including products from Fidelity, Bitwise, and Ark 21Shares. MIAX followed suit in late January. At this point, nearly every regulated venue in the U.S. has lined up behind the same framework.

What Actually Changed

The 25,000-contract limit was always seen as a temporary measure – a way to keep a lid on volatility while regulators got comfortable with a new asset class. Its removal signals something more permanent: crypto ETFs are now treated like gold or oil trusts, not like speculative instruments that need extra supervision.

Beyond the raw numbers, the rule change opens the door to FLEX options. These are customizable contracts – institutional investors can set their own exercise prices and expiration dates, replicating the kind of flexibility that previously existed only in over-the-counter markets. NYSE Arca has also updated rules to permit cash-settled FLEX options for IBIT and similar products, which matters to institutions that have no interest in dealing with physical ETF share delivery at settlement.

The SEC’s broader shift here is worth noting. The agency has moved away from approving each new crypto-linked product on a case-by-case basis. Generic listing standards now apply, meaning exchanges like Nasdaq and Cboe BZX can run through a checklist-style review for new products rather than waiting on individual sign-off. Regulators are no longer treating these funds as a special category requiring unusual scrutiny.

The Numbers Behind the Move

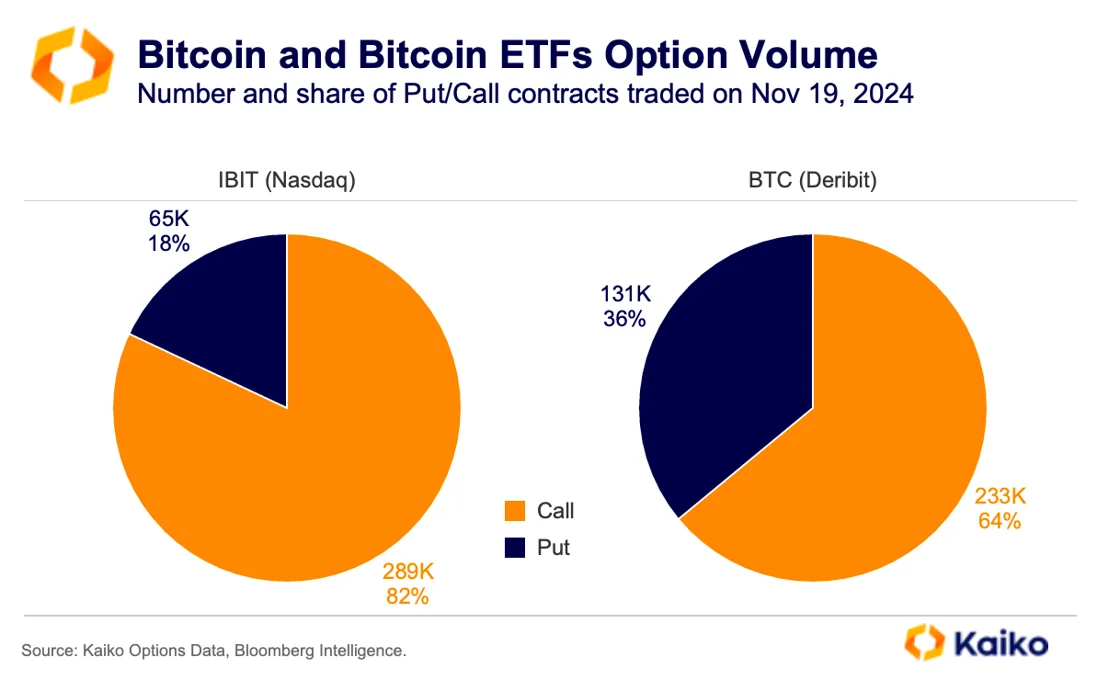

When IBIT options first launched in November 2024, the market’s appetite was immediate – $1.9 billion in notional volume on day one, according to Kaiko research. More than 80% of that was call options, a clear sign of bullish sentiment. The volume was there from the start; the constraints were regulatory, not structural.

Galaxy Digital had previously forecast that spot Bitcoin ETFs would pull in $14.4 billion in their first year. The availability of more sophisticated hedging tools now in place makes that kind of institutional inflow more plausible, not less. Standard Chartered, for its part, has maintained a long-term bullish view on Ethereum, with price projections ranging from $10,000 to $40,000 – and has pointed to derivatives market development as a meaningful catalyst.

What It Means for the Market

The optimistic case is straightforward: more institutional participation means more competition between market makers, which typically compresses spreads. Deeper liquidity means retail orders are less likely to move the price against themselves. FLEX options give hedgers more precise tools, and when hedgers manage their own risk more efficiently, those savings tend to flow downstream.

The implied volatility picture is more complicated. Historically, when position limits are lifted on liquid ETFs, pricing efficiency improves and volatility shocks tend to moderate over time. Institutions running yield-enhancement strategies – selling covered calls, for instance – add supply to the options market, which puts downward pressure on implied volatility and makes premiums cheaper for retail buyers. The flip side is that high short-dated demand from retail traders, especially around major market events, can still trigger localized IV spikes.

There’s also a structural concern worth flagging. Some analysts argue that removing position limits increases the amount of “paper” Bitcoin in circulation – derivatives exposure rather than direct ownership of the underlying asset. If institutions increasingly access Bitcoin through options rather than spot, that could have implications for price discovery and the spot market’s depth.

The Bigger Picture

What happened here isn’t just a rule change. It’s the final stage of a normalization process that started when spot Bitcoin ETFs were approved and has been moving steadily since. The infrastructure – the listing standards, the position frameworks, the settlement mechanics – now looks essentially identical to what exists for commodity ETFs. That wasn’t true a year ago.

Nasdaq and CME Group announced a joint crypto index in early 2026 covering Bitcoin, Ether, XRP, and Solana, intended to serve as the foundation for future multi-asset crypto ETF options. The derivatives market for digital assets is being built out deliberately, piece by piece, and the position limit removal is the clearest signal yet that regulators aren’t planning to reverse course.

Whether that’s good or bad depends on what you think about institutional involvement in crypto markets. The optimists see deeper liquidity and better pricing. The skeptics see leverage, paper supply, and the kind of short-term volatility that comes with large contract expirations. Both are probably right, at different moments.

The information provided in this article is for educational purposes only and does not constitute financial, investment, or trading advice. Coindoo.com does not endorse or recommend any specific investment strategy or cryptocurrency. Always conduct your own research and consult with a licensed financial advisor before making any investment decisions.

The post NYSE Removes Position Limits on Bitcoin and Ether ETF Options – What Actally Changed appeared first on Coindoo.

Source: https://coindoo.com/nyse-removes-position-limits-on-bitcoin-and-ether-etf-options-what-actally-changed/

More Crypto News

Check our Market Overview

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research (DYOR).